Mortgage Interest Rates Today: Rates Rise to 6.11% as Iran War Sparks Oil Shock

Mortgage rates rose on Thursday to their highest level in five weeks as volatility in the markets caused by the ongoing war in Iran outweighed relatively tame data on jobs and inflation.

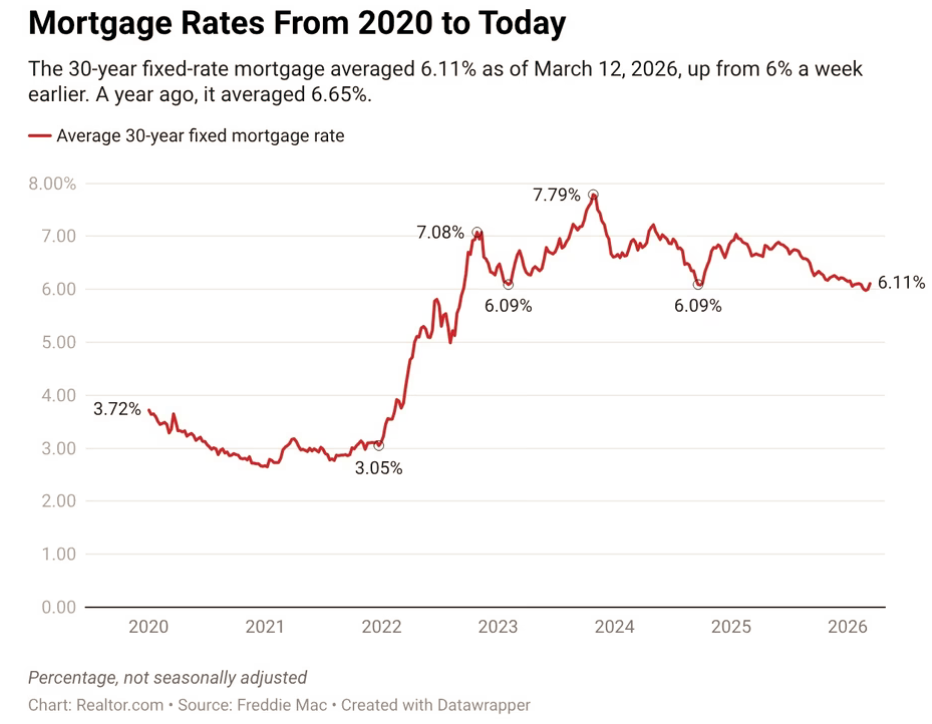

The average rate on 30-year fixed home loans jumped to 6.11% for the week ending March 12, up 11 basis points from 6% the week before, the largest weekly increase since April 2025, according to Freddie Mac. For perspective, rates averaged 6.65% during the same period in 2025.

"The 30-year fixed-rate mortgage returned to last month’s level of 6.11%," said Sam Khater, Freddie Mac's chief economist. "Despite the modest uptick, buyers are responding to rates in this range, with existing-home sales increasing 1.7% in February. Purchase applications also increased this week, a welcome sign as buyers enter spring homebuying season with rates down more than half a percentage point compared to the same time last year."

Escalating unrest in the Middle East, marked by Iranian missile and drone attacks on targets across the Gulf region, including oil tankers, has stoked fears of wartime inflation as crude prices soared. The resulting sell-off in the bond market sent yields on the 10-year Treasury climbing, driving mortgage rates higher this week.

Realtor.com® senior economic research analyst Hannah Jones says this shift comes despite last week’s weaker-than-anticipated jobs data, with unemployment in February ticking up to 4.4% and nonfarm payrolls shrinking by 92,000 jobs.

Inflation also drifted lower last month, with headline inflation holding steady at 2.4% and core inflation at 2.5%.

"Under normal circumstances, these soft economic readings would put downward pressure on mortgage rates," says Jones. "However, the news out of the Middle East is overriding those signals."

The analyst points out that the current sense of unease coursing through the housing market echoes the tariff-fueled volatility that disrupted financial markets this time last year.

"While the 2025 spring season didn't culminate in a full-scale recession, the sheer weight of macro-uncertainty was enough to stifle what should have been a period of growth," says Jones.

As the Federal Reserve shifted to a "wait-and-see" stance on future interest rate cuts and consumer confidence weakened, many prospective homebuyers retreated to the sidelines, resulting in one of the most sluggish housing years in recent memory.

The new year began with a window of opportunity for buyers, as mortgage rates dipped to their lowest levels in more than three years and February pending sales climbed 2.4% year over year.

"However, the sudden injection of geopolitical friction threatens to curb that enthusiasm," adds Jones. “For the market to sustain its 'pep,' buyers require more than just favorable borrowing costs. They need the psychological green light provided by a stable economic outlook."

How mortgage rates are calculated

Mortgage rates are determined by a delicate calculus that factors in the state of the economy and an individual’s financial health. They are most closely linked to the 10-year Treasury bond yield, which reflects broader market trends like economic growth and inflation expectations. Lenders reference this benchmark before adding their own margin to cover operational costs, risks, and profit.

When the economy flashes warning signs of rising inflation, Treasury yields typically increase, prompting mortgage rates to increase. Conversely, signs of falling inflation or weakness in the labor market usually send Treasury yields lower, causing mortgage rates to fall.

The mortgage rates you’re offered by a lender, however, go beyond these benchmarks and take some of your personal factors into account.

Your lender will closely scrutinize your financial health—including your credit score, loan amount, property type, size of down payment, and loan term—to determine your risk. Those with stronger financial profiles are deemed as lower risk and typically receive lower rates, while borrowers perceived as higher risk get higher rates.

How your credit score affects your mortgage

Your credit score plays a role when you apply for a mortgage. A credit score will determine whether you qualify for a mortgage and the interest rate you'll receive. The higher the credit score, the lower the interest rate you'll qualify for.

The credit score you need will vary depending on the type of loan. A score of 620 is a "fair" rating. However, people applying for a Federal Housing Administration loan might be able to get approved with a credit score of 500, which is considered a low score.

Homebuyers with credit scores of 740 or higher are typically considered to be in very good standing and can usually qualify for better rates.

Different types of mortgage loan programs have their own minimum credit score requirements. Some lenders have stricter criteria when evaluating whether to approve a loan. They want to make sure you're able to pay back the loan.

Source Realtor.com